Strategy’s STRC preferred stock is fueling a sharp debate across crypto markets. Analysts are divided over whether the high-yield instrument echoes the dynamics that destroyed TerraUSD (UST) in 2022.

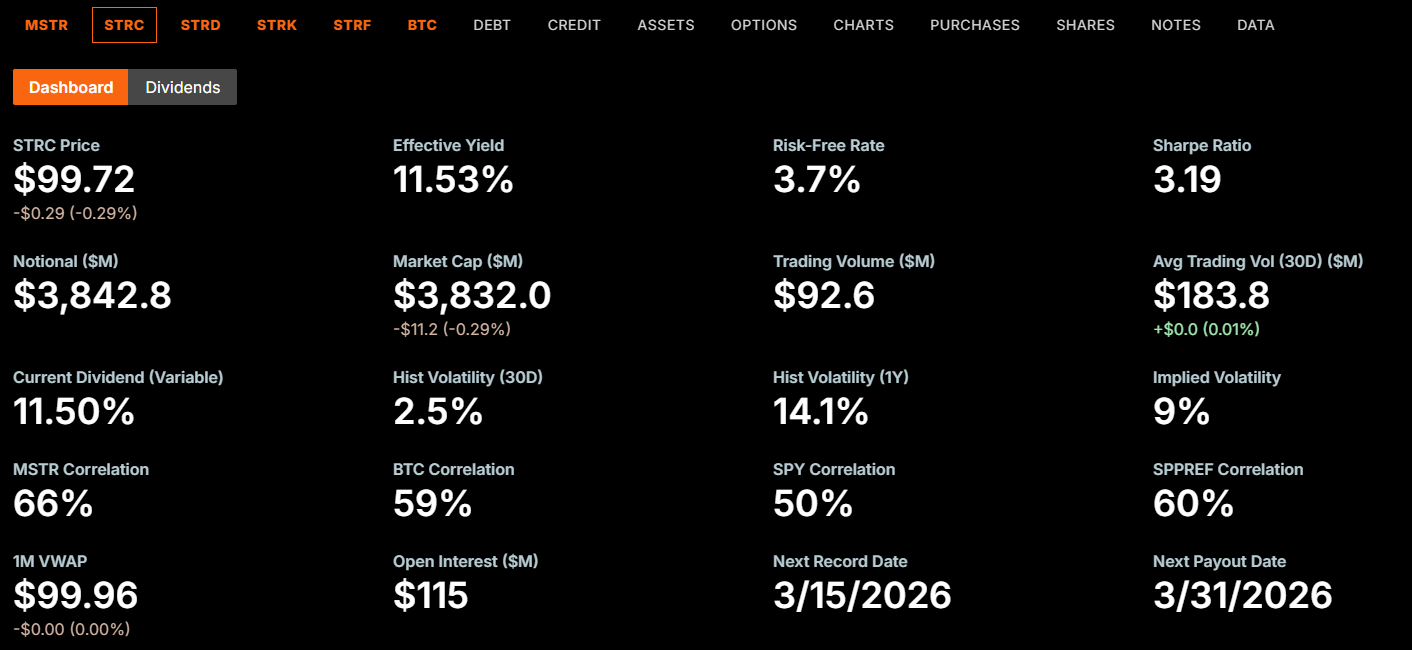

The variable-rate perpetual preferred stock, known as “Stretch,” currently pays an annualized dividend of 11.5% on a $100 par value. The yield has climbed steadily since STRC launched in July 2025 at 9%, drawing comparisons to the unsustainable returns that once powered Terra’s growth. Because nothing says “sustainable finance” like a yield so high it makes your eyes water.

How Terra Actually Collapsed

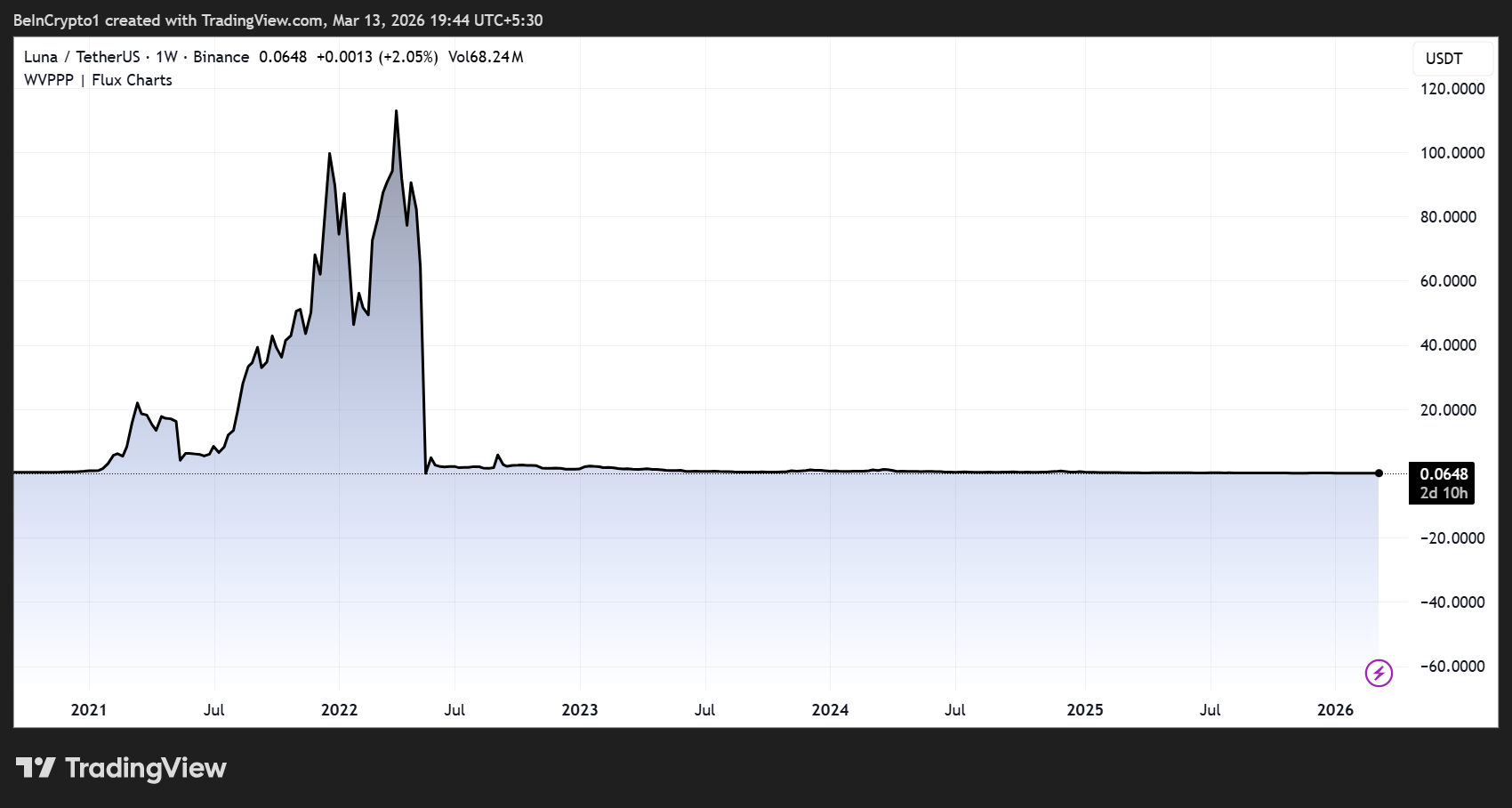

Understanding whether the comparison holds requires examining how UST’s failure mechanism worked. Terra’s system relied on an algorithmic mint-and-burn loop between UST and its sister token Luna (LUNA). A financial house of cards dressed in code, if you will.

The Anchor lending protocol offered depositors yields near 20%, attracting billions in capital. When confidence broke in May 2022, UST holders rushed to redeem their tokens for LUNA. Classic: “Oh no, my stablecoin isn’t stable anymore. Let me just exchange it for whatever this other thing is.”

Each wave of redemptions minted new LUNA, flooding its supply and crashing its price. That falling price further eroded confidence in UST’s backing, triggering more redemptions and more LUNA minting. A self-reinforcing death spiral, or as we like to call it, “the crypto version of a rom-com where everyone breaks up.”

The result was a self-reinforcing death spiral that wiped out roughly $45 billion in market value within days. Do Kwon, Terra’s founder, was later sentenced to 15 years in federal prison for fraud tied to the collapse. A fittingly tragic ending to a soap opera that even daytime TV would shy away from.

The critical detail is that Terra’s destruction was mechanical. The protocol itself generated hyperinflation through its own redemption design, and no board, regulator, or circuit breaker could stop it once the loop accelerated. Like a toaster that’s also a time bomb.

Where the STRC Comparison Holds and Where It Breaks

STRC shares one structural feature with Terra. Both create a feedback loop in which attractive yields draw capital, that capital flows into an underlying asset, and the asset’s perceived strength attracts more capital. Same song, different verse. If this sounds too good to be true, it probably is.

“STRC is pretty much UST all over again. Enjoy the yield while it lasts,” wrote Wazz. Because nothing says “financial innovation” like repeating history with a new name.

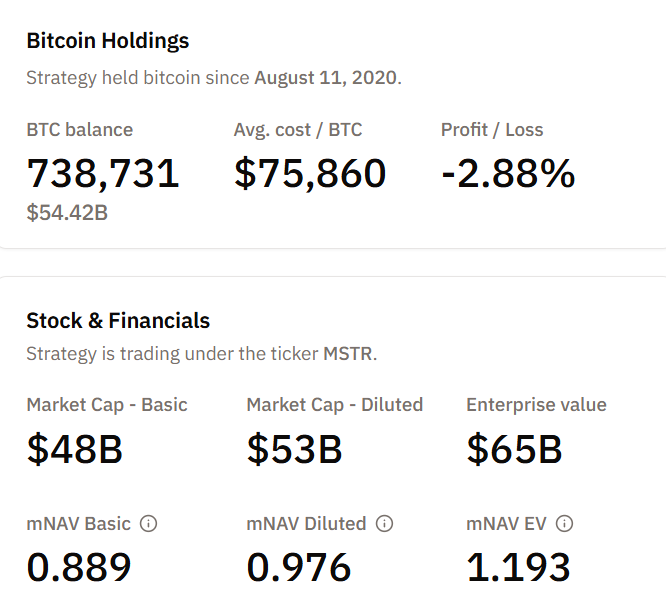

However, the failure mechanisms are fundamentally different. UST had a protocol-level redemption loop that could automatically mint unlimited LUNA tokens. STRC has no such mechanism. It is a corporate preferred stock issued by Strategy, backed by 738,731 BTC on the company’s balance sheet as of March 13. Oh, how progressive.

There is no algorithmic trigger that can hyperinflate a token supply in response to selling pressure. Phew. That’s one less thing to panic about.

“It is literally nothing like $UST as it’s backed by Bitcoin on the balance sheet in the cap structure… Literally cannot happen. What can happen is Bitcoin not going up…” trader Farmer Joe challenged. Because that’s never happened before, right?

In other words, STRC cannot death-spiral the way UST did. However, that does not mean it carries no risk. The comparison highlights a real vulnerability, even if the worst-case outcome looks different. Like a teetering Jenga tower made of Bitcoin and hope.

The Risks That Remain Without a Death Spiral

Analyst Colin Talks Crypto recently shared a detailed risk breakdown, noting that STRC’s board declares dividends monthly and can slash or suspend them at any time. The stock has no hard price floor, no maturity date, and no FDIC insurance. It sits junior to corporate debt and Strategy’s STRF preferred series in the capital structure. A luxury resort for investors who hate guarantees.

“STRC doesn’t really give you any guarantees (despite seeming like guaranteed fixed income), and it absolutely DOES carry risks…” wrote Colin. Because nothing’s riskier than a “guaranteed yield” that isn’t actually guaranteed.

Strategy can also issue unlimited new STRC shares through at-the-market offerings without shareholder approval. In early March alone, the company sold 3.7 million STRC shares, raising $377 million to fund further BTC purchases. That growing obligation creates a fixed-cost burden that must be serviced indefinitely. Like a mortgage for a house you can’t afford, but in Bitcoin.

Strategy has acquired 17,994 BTC for ~$1.28 billion at ~$70,946 per bitcoin. As of 3/8/2026, we hodl 738,731 $BTC acquired for ~$56.04 billion at ~$75,862 per bitcoin. $MSTR $STRC

– Strategy (@Strategy) March 9, 2026

With Bitcoin trading just above $73,000, Strategy’s portfolio carries substantial unrealized losses against its average cost basis of roughly $75,860 per coin. If BTC enters a prolonged decline, the company faces shrinking collateral value while dividend obligations continue to grow with each new STRC issuance. The feedback loop would not produce a Terra-style instant wipeout. However, it could produce a slow squeeze of

- Dividend cuts

- Price drops below par, and

- Eroding investor confidence.

Bulls See a New Credit Benchmark, Not a Time Bomb

Adam Livingston, a vocal STRC advocate, described the instrument as a coupon-bearing rail that absorbs fixed-income demand, converts it into BTC at scale, and feeds an equity premium that makes each subsequent capital raise cheaper. Or, as we like to call it, “the crypto equivalent of a Ponzi scheme with a better PR team.”

🚨HOW $STRC IS EATING THE WORLD – EXPLAINED!🚨

STRC is quietly turning Strategy into a private central bank for the yield-starved world, except the collateral base is a growing Bitcoin hoard and the issuance is a publicly traded instrument that Wall Street can actually buy.…

– Adam Livingston (@AdamBLiv) January 14, 2026

He argued STRC competes with junk credit while avoiding refinancing cliffs, maturity walls, and covenant restrictions. Livingston also pointed to what he called 75 years of dividend coverage on the balance sheet. A bold claim, especially when the balance sheet is basically a Bitcoin piggy bank with a few zeros tacked on.

Strategy chairman Michael Saylor announced in late 2025 that the STRC dividend would reach 11% in January 2026.

Stretch goes to 11% in January 2026. $STRC

– Michael Saylor (@saylor) January 1, 2026

CEO Phong Le said in February that the company plans to pivot from common stock issuance toward preferred capital as its primary fundraising tool.

Recent developments indicate sales of up to 2,034 MSTR shares from restricted stock vesting.

JUST IN: Strategy’s CEO Phong Le has sold 2,034 $MSTR shares from restricted stock vesting at an average price of $137.25 for $279,174, according to the recent form 144 filing.

– BitcoinTreasuries.NET (@BTCtreasuries) March 13, 2026

So Is the Comparison Fair?

Partially. The Terra analogy correctly identifies STRC’s dependence on a capital inflow cycle tied to a volatile underlying asset. Both instruments used high yields to attract capital that reinforced the asset base, and both face stress if that cycle reverses. However, the comparison overstates the risk of catastrophic collapse.

- UST failed through an automated, self-reinforcing hyperinflation mechanism that no human decision could halt.

- STRC is a corporate security with a board that controls dividend policy, a real Bitcoin treasury, and no protocol-level death spiral trigger.

Perhaps, the worst plausible outcome for STRC is painful but bounded, such that:

- Dividends get cut,

- The stock falls below par, and

- Investors take losses on what turned out to be high-risk equity rather than stable income.

The deeper question is whether investors buying STRC at 11.5% understand they hold a Bitcoin bet wrapped in a yield product, not a fixed-income instrument with guaranteed returns. Or, to put it another way: if you’re buying a “safe” yield, maybe check the fine print. It might say “not safe at all.”

Read More

- Gold Rate Forecast

- Silver Rate Forecast

- TRX: The Bullish Saga of $0.30 – Will the Whales Save Us? 🐋💰

- France’s Fiendish Plot to Fry Crypto Exchanges in a Pot of Regulation Soup 🧙♂️🔥

- Bitcoin’s Wild Ride: $85K or Bust! 🚀📉

- Discover the Bizarre Fate of Bitcoin: Fortune or Folly? 😏

- Crypto Listings Fail: Market Dives in Disgrace 🚀💸

- Tangem Wallet Adds Aave Yield – But Is It Magic Or Just Marketing? 🤔💸

- Crypto Comes to Shopify! Merchants Rejoice or Panic? 🎉💸

- Bitcoin’s Bold $112K Move – Is It A Breakout Or A Breakdown? Find Out! 💥💸

2026-03-13 18:07