Ah, stablecoins… a rather curious phenomenon, wouldn’t you say? A digital attempt to tame the volatile beast of cryptocurrency, and now, a force accumulating a sum—two hundred and sixty billion dollars, if you please—that even the most seasoned financiers are forced to acknowledge. It’s enough to make one raise an eyebrow, and perhaps mutter something about the folly of man.

- The Americans, in their typically pragmatic fashion, have passed a law—the GENIUS Act, no less—attempting to corral these digital steeds with a set of rules. A grand undertaking, to be sure.

- Banks and grand corporations, always seeking a new field to graze in, are circling. JPMorgan, Citigroup, Amazon, even Walmart! The scent of profit is strong, it seems.

- These stablecoins are now buying up American Treasury bonds with such zeal that they’ve become significant holders of the national debt. A rather unsettling thought, wouldn’t you agree?

- The world’s regulators, predictably, are wringing their hands and issuing warnings. Liquidity, redemption, systemic risk… the usual litany of anxieties.

Table of Contents

A Federal Rulebook Emerges

For a long time, the notion of a privately issued digital currency operating alongside the established banking system was considered, shall we say, a bit fanciful. But then came July of 2025, and President Trump, with a characteristic flourish, signed the GENIUS Act into law. And so, the first official framework for stablecoins in the United States was born.

The GENIUS Act – an acronym as inventive as its subject matter, Guiding and Establishing National Innovation for U.S. Stablecoins – grants these digital creations a certain… legitimacy. They are not to be confused with securities, nor are they bank deposits. Simply “digital instruments,” they are proclaimed, moving money with a level of trust and reliability. One wonders if such trust is truly warranted.

The bill, surprisingly, passed with bipartisan support – a rare occurrence these days. Apparently, even politicians can recognize the need for modernization. Licensed issuers—banks, credit unions, and various fintech firms—are now permitted to issue these dollar-backed stablecoins.

And the rules? Rigid, they are. Each stablecoin must be backed one-to-one by U.S. dollars or short-term Treasury bills. Reserves must be segregated, audits performed, and monthly reports published for public scrutiny. A commendable level of transparency, though one suspects much will still remain hidden from view.

Oversight, naturally, depends on size. The larger players—those exceeding $10 billion in circulation—will face the scrutiny of the Office of the Comptroller of the Currency, the Federal Reserve, and the FDIC. The smaller ones, for now, remain under the watchful eyes of state regulators, until, inevitably, they too grow beyond that threshold.

Algorithmic stablecoins, those prone to spectacular collapses, are explicitly excluded. And, rather drily, issuers are prohibited from offering yield or interest on these tokens. The specter of TerraUSD, it seems, still haunts the halls of power.

Analysts predict that these new rules will encourage wider adoption. Standard Chartered estimates a potential rise to $2 trillion by 2028. Such optimism is typical of analysts, wouldn’t you agree? It may encourage banks to adopt digital dollars, and perhaps even increase the demand for Treasury assets.

Wall Street and Retail Giants Step In

The scent of regulation, it appears, has awakened the giants of finance. JPMorgan Chase, under the leadership of the ever-pragmatic Jamie Dimon, has announced the piloting of a new blockchain-based product: JPMorgan Deposit Token, or JPMD. It’s a bridge between the old and the new, they say.

Unlike JPM Coin, which operates in a private network, JPMD is designed for the public blockchain. Dimon, despite his long-held skepticism towards cryptocurrency, has admitted the bank intends to engage with stablecoins to, as he put it, “understand the technology.” A cautious approach, and a sensible one, perhaps.

Citigroup, not to be outdone, is also exploring its options. CEO Jane Fraser speaks of reserve management, potential stablecoin issuance, and custody solutions. And other major banks—Bank of America, Wells Fargo, Goldman Sachs—are reportedly considering a shared infrastructure, similar to Zelle’s instant payment network.

Even the retail sector is stirring. Amazon, Alibaba, and Walmart are all contemplating launching their own dollar-backed stablecoins, primarily to reduce those pesky payment processing costs. U.S. merchants paid over $187 billion in interchange fees in 2024! A considerable sum, indeed.

And so, the inexorable march of technology continues. The potential for stablecoins extends to cross-border payments, supply chain finance, and corporate disbursements. The world is changing, whether we like it or not.

Stablecoins are now deeply embedded in the U.S. debt

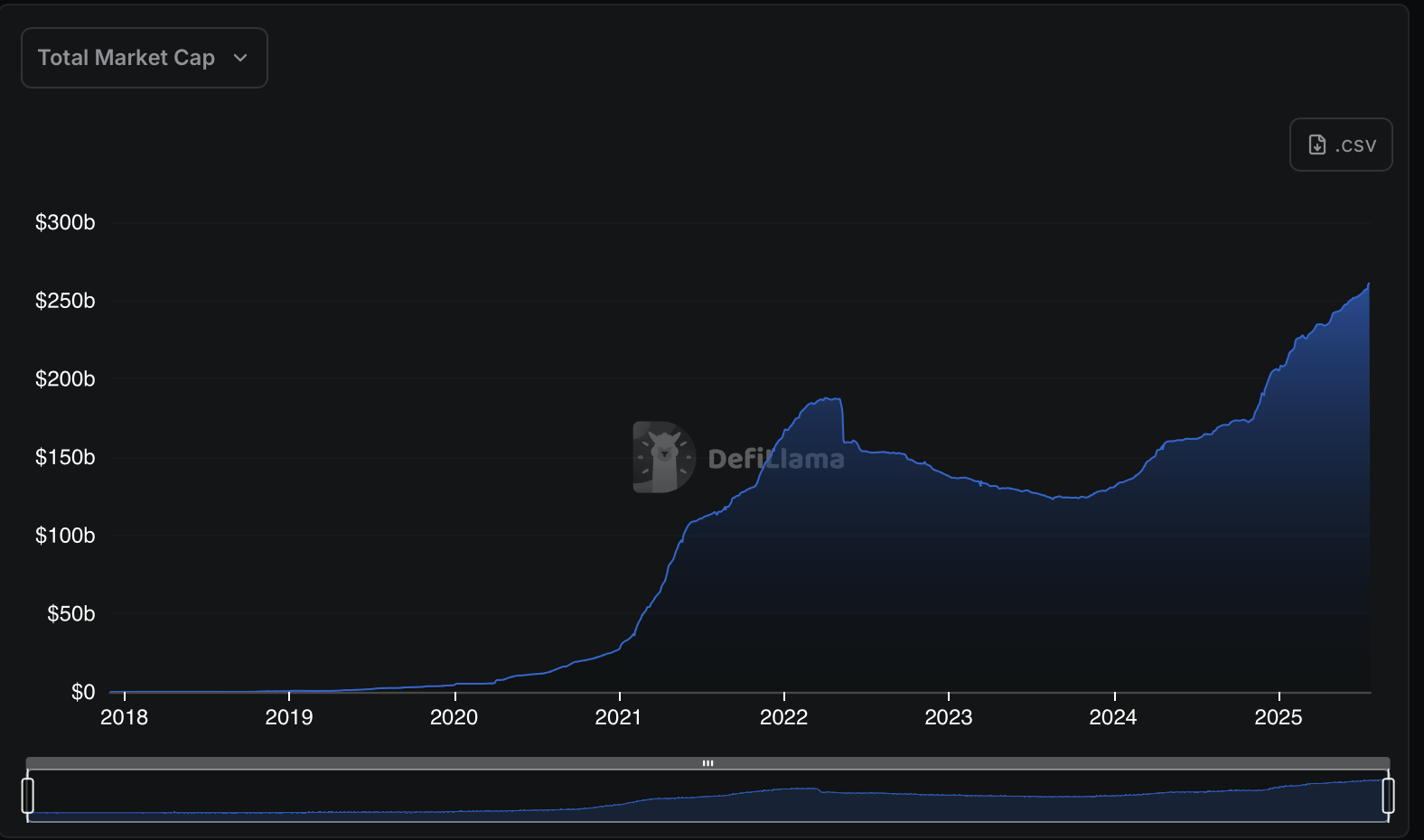

The stablecoin market now stands at approximately $263 billion – a rather staggering 50-fold increase over the past five years.

This growth is driven by a desire for stability in the volatile world of crypto and a closer connection to traditional financial systems. Eighty to ninety percent of stablecoin reserves are now held in short-term U.S. Treasury instruments, equating to over $200 billion in Treasury exposure!

Morgan Stanley projects a market size of $750 billion by 2026. Such a market could actively influence Treasury market dynamics. It’s enough to give a Treasury Secretary pause, wouldn’t you say?

Officials, like Treasury Secretary Scott Bessent, acknowledge that stablecoins have helped the Treasury manage funding more flexibly. They have contributed to a compression of yields on short-term government debt, effectively reducing borrowing costs. A convenient arrangement, to be sure.

Sound money or shadow risk?

The integration of stablecoins is accelerating, but questions linger. The Bank for International Settlements, never one to mince words, has declared that stablecoins do not yet meet the standards of “sound money.” Singleness, elasticity, and integrity – the usual concerns.

The BIS also points to the impact on the U.S. Treasury market. Every $3.5 billion increase in stablecoin issuance could reduce Treasury yields by up to 5 basis points. A seemingly small effect, perhaps, but one that could accumulate over time.

The potential for drawing funds from traditional bank deposits is another worry. Estimates suggest up to $6.6 trillion could be diverted, potentially shrinking the capital available to lenders. A rather gloomy prospect.

The collapse of USDC in March 2023, triggered by its exposure to Silicon Valley Bank, serves as a stark reminder of the fragility of this structure. A loss of peg, redemptions of over $4 billion… a rather unpleasant episode.

Compliance and enforcement remain challenging. Pseudonymous, cross-border transfers complicate anti-money laundering efforts. And the lack of central bank guarantees adds to the uncertainty.

Regulatory bodies are scrambling to formulate frameworks. The Financial Stability Board, the BIS, and central banks like the Bank of England are all involved. The consensus seems to be regulation under strict supervision, but not a replacement for sovereign currencies.

The future of stablecoins remains uncertain. Transparency, audits, and coordinated regulation will be crucial in establishing credibility and safety. Without them, they may remain a niche curiosity. With them… well, who knows? Perhaps they will become a foundational component of digital finance, for better or for worse.

Read More

- ETH PREDICTION. ETH cryptocurrency

- Gold Rate Forecast

- Silver Rate Forecast

- Brent Oil Forecast

- Sui’s USDsui: The Stablecoin That’ll Make Your Wallet Go “Oh, That’s Nice!” 🚀💸

- USD THB PREDICTION

- Bitcoin Beats Silicon Valley: The Unlikely Hero of 2023 🚀

- Ethereum’s ETH: The New Global GDP? 🌍💰

- 5 Crypto Tokens to Watch in 2025: One with a TradFi Twist 🚀💰

- Apple’s Brilliant iPhone Escape Plan: India vs. Tariffs! 🤯

2025-07-23 22:27