Pools of Opportunity: How Aggregators Make Stabull the Belle of DeFi’s Ball

The ninth delightful installment in our 15-part “Deconstructing DeFi” Series.

The ninth delightful installment in our 15-part “Deconstructing DeFi” Series.

A crypto analyst believes the recent price drop wasn’t just a temporary setback, but a signal that the price is still likely to fall further. This puts the price in a vulnerable position, and another drop could lead to it falling as low as $0.75.

A slowdown, they say, from the frenzied tempo of recent weeks. The first two days, a crescendo of $635 million, only to be silenced by the FOMC’s stern baton, conducting a sharp reversal of $405 million. By Friday, the melody softened, but the discord remained.

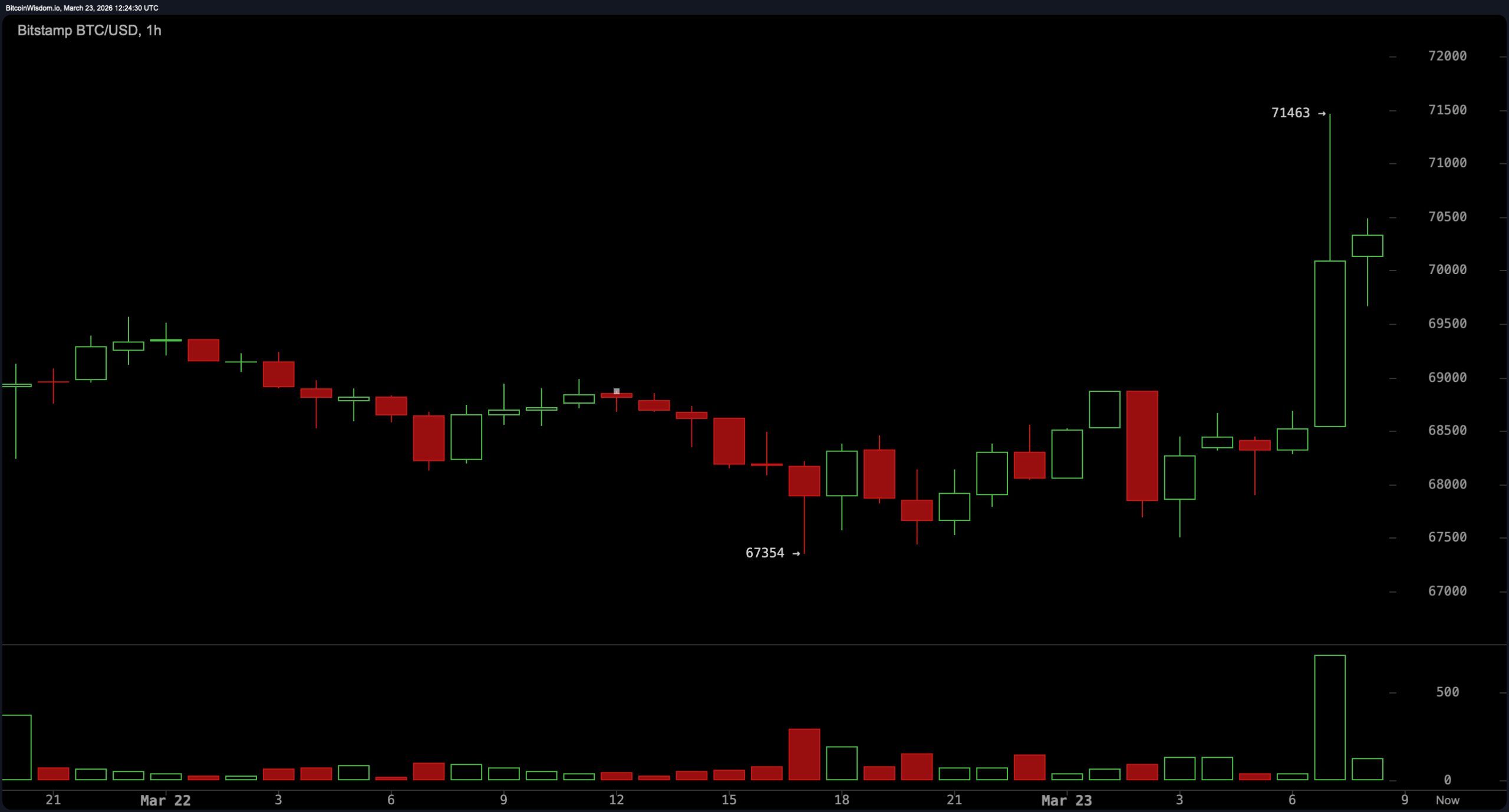

Looking at the daily chart, Bitcoin is currently moving within a clear downward trend channel. Both its 100-day and 200-day moving averages are trending downwards, around $80,000 and $92,000 respectively. The $75,000 to $80,000 price range, which previously supported the price for much of late 2025, is now acting as a resistance level, and every attempt to push the price higher since February has failed at this point.

According to the oracle known as CoinShares, the digital asset exchange-traded products managed to haul in a mere $230 million last week, extending their positive spell to four weeks. But do take note, this figure is a far cry from the luxurious $1.06 billion that graced the records just a week prior. Investor enthusiasm appears to have taken a much-needed vacation.

This delightful upward trajectory followed Trump’s grand announcement, where he claimed to have engaged in some high-level chitchat with Iran-apparently, their conversations were so productive they could rival the negotiations of a second-rate soap opera. He proclaimed a five-day ceasefire on his military plans against Iranian energy infrastructure, as if he were calling off a picnic after realizing it might rain.

In the dusty fields of the financial plains, where the winds of volatility howl and the sun of speculation beats down mercilessly, a man stands tall-or at least, he pretends to. Michael Saylor, the ringmaster of Strategy, has once again thrown his hat into the ring, stacking another 1,031 BTC for a cool $76.6 million. That’s $74,326 per coin, if you’re keeping score at home. And keep score you should, because this circus has more numbers than a CPA’s wet dream.

Yet, the on-chain data, that inscrutable oracle of modern times, tells a tale as contradictory as a Wildean paradox. What are these miners doing with their coins, one might ask? Hoarding them, it seems, like misers clutching at pearls in a storm.

Bitcoin bulls should be on their toes: A key momentum indicator that has been disturbingly accurate at flagging selloffs since the largest cryptocurrency hit a record high in October has just triggered. It’s like a ticking time bomb dressed in a tuxedo-sleek, sophisticated, and ready to blow.

The underlying asset attempted a notable breakout during the week, only to be rejected and driven south toward its starting position. It’s like a toddler trying to climb a mountain only to realize the summit is just a pile of sand and a misplaced snack.