Ah, the golden age of capitalism! Or so Daniel Oliver, the sage of Myrmikan Capital, would have us believe. In a recent interview, this modern-day Cassandra foretold the end of gold’s serene ascent and the dawn of a tempestuous era in U.S. private credit. Brace yourselves, comrades, for the markets are about to get as turbulent as a Bolshevik rally!

Margin Calls and Maturity Walls: Gold’s New, Slightly Hysterical Reality

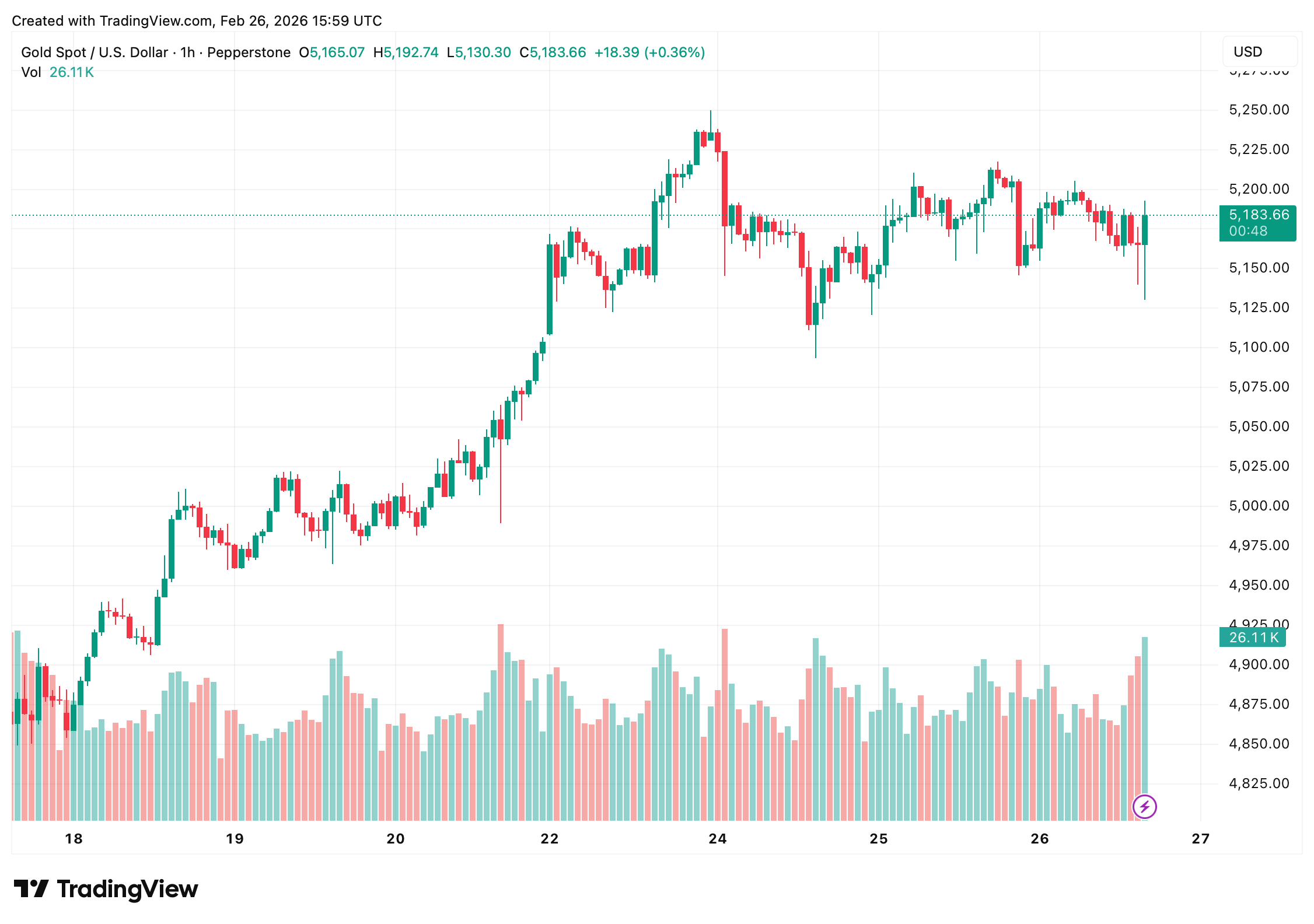

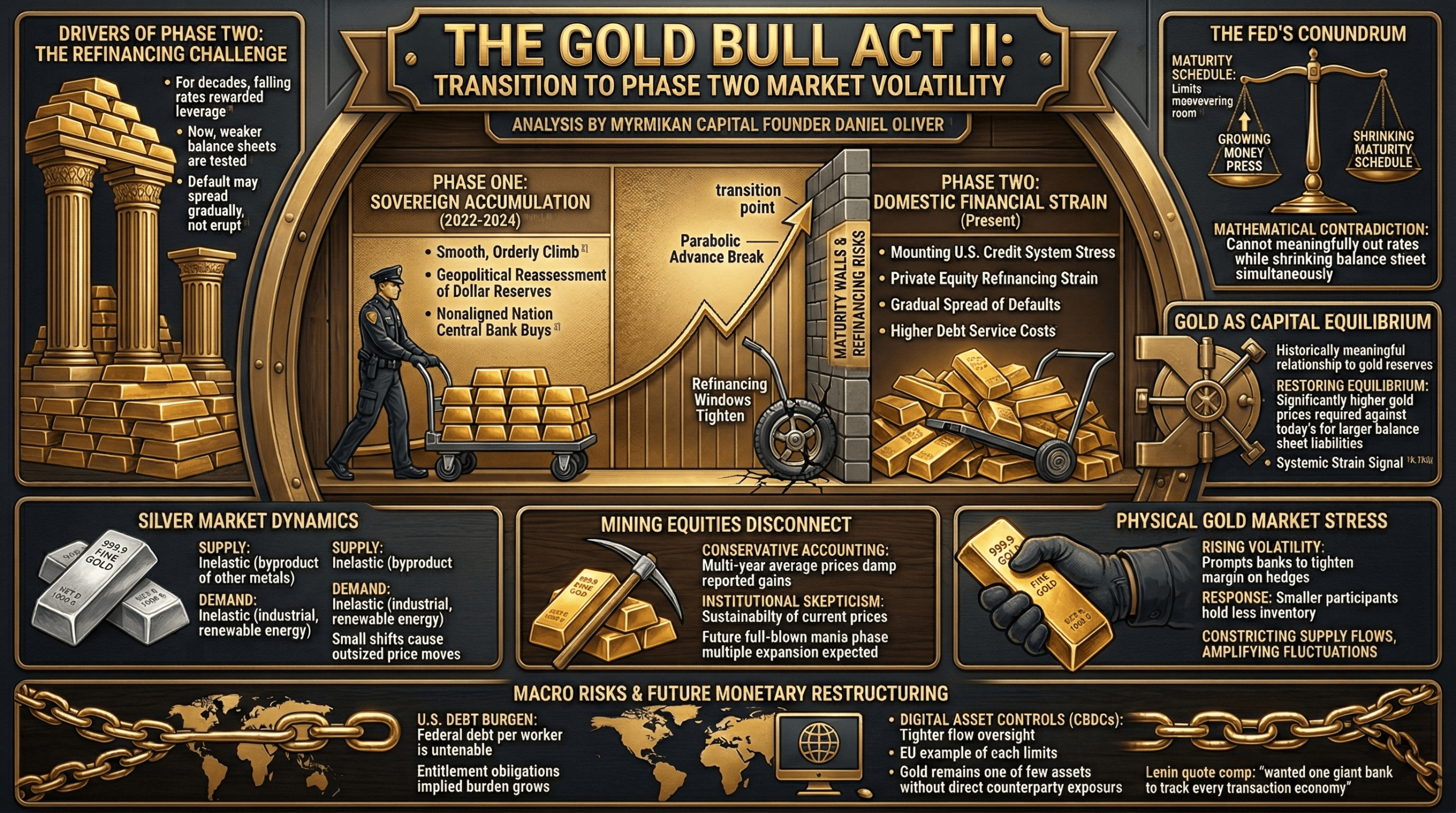

In a conversation with Kitco News’ Jeremy Szafron, Oliver proclaimed the end of gold’s smooth, sovereign-driven accumulation phase. Since 2022, central banks have been hoarding gold like squirrels with a nut obsession, but now, he warns, the party’s over. Enter phase two: a volatile, credit-crunched circus powered by the U.S. financial system’s mounting stress, private equity’s refinancing roulette, and a Federal Reserve juggling maturity schedules like a clown with too many plates.

Phase one, Oliver explains, began when geopolitical tensions in 2022 made nonaligned nations rethink their dollar reserves. Central banks started buying gold like it was going out of style, unbothered by price swings. This steady institutional binge sent gold on a stately climb, as orderly as a Tsarist ball. But now, the music has stopped, and the dance floor is chaos.

“If you look at the chart,” Oliver quipped, “gold painted a lovely parabola until a few weeks ago, when it decided to break into a frenzied jig.”

At the heart of this drama? Private equity and credit, of course. For decades, falling interest rates rewarded leverage like a capitalist fairy tale. Funds borrowed like there was no tomorrow, acquired companies, and refinanced at lower costs. But now, with rates higher than a Bolshevik’s ideals, weaker balance sheets are cracking. Companies that once rolled debt forward with ease now face costs that would make even a tsar blush.

Oliver predicts defaults won’t erupt like a 2008 fireworks display but will spread gradually, like a slow-burning revolution. The Federal Reserve, meanwhile, is in a bind. Can it lower rates while shrinking its balance sheet? Oliver scoffs at the idea, calling it “mathematically absurd.” If credit markets seize, he expects the Fed to print money like it’s 1917 Petrograd.

“We know the Fed’s solution to a crisis,” Oliver remarked, “is to print more money than a counterfeiter on a bender.”

This, naturally, plays right into gold’s hands. Oliver sees gold as the ultimate counterbalance to central bank liabilities. Historically, central bank balance sheets had a cozy relationship with gold reserves. Today, with the Fed’s balance sheet bloated like a capitalist after a feast, gold prices would need to soar to restore equilibrium. Capitalism, it seems, demands its pound of flesh-or should we say, ounce of gold?

Silver, meanwhile, is having its own moment. Most silver production is a byproduct of other metals, making supply as inflexible as a bureaucrat’s mind. Demand, driven by industrial uses and renewable energy, is equally stubborn. When both supply and demand are inelastic, small shifts cause price moves that would make a speculator’s heart race.

Even the physical gold market is under strain. Traders and refiners, usually hedged through futures, are now facing tighter margin requirements from banks. Smaller players may reduce inventory or throughput, constricting supply and amplifying price swings. It’s a game of musical chairs, and the music is getting louder.

Despite gold’s strength, mining equities are lagging. Oliver blames conservative accounting and institutional skepticism about gold’s sustainability. Large companies value reserves using multi-year average prices, muting reported gains. But in a full-blown mania, he predicts, valuation multiples will expand like a revolutionary’s dreams.

Beyond markets, Oliver paints a grim fiscal picture. U.S. federal debt, when divided among workers, is economically untenable. Add long-term entitlement obligations, and the burden grows heavier. Monetary restructuring-inflationary, negotiated, or otherwise-seems inevitable. It’s enough to make one nostalgic for simpler times, like the collapse of the Romanov dynasty.

Oliver also warns about the digitization of money and potential financial controls. Governments, he notes, historically tighten oversight during instability. Physical gold, he argues, remains one of the few assets without direct counterparty exposure. “Governments love digital currencies,” he said, “because they can track every transaction. It’s like Lenin’s dream of one giant bank-except the EU doesn’t realize they’re quoting him.”

For viewers, the message is clear: gold’s next phase won’t be a serene climb but a wild ride shaped by credit stress and policy limits. Whether it’s a slow grind or a sharp repricing depends on the private credit cycle and the Fed’s response. In Oliver’s view, gold is already signaling strain-and the second act of this bull market has begun. Fasten your seatbelts, comrades, for the revolution in finance is here.

FAQ 🔎

- What does Daniel Oliver mean by gold’s “phase two”?

He describes a shift from central bank-driven accumulation to volatility fueled by U.S. credit stress and private equity’s refinancing woes. - Why does Oliver believe the Federal Reserve is constrained?

He argues the Fed can’t cut rates and shrink its balance sheet without destabilizing liquidity-a capitalist’s Catch-22. - How could private credit affect gold prices?

Rising defaults and refinancing pressure could force monetary easing, which gold markets are already pricing in. - Why are gold miners underperforming bullion?

Oliver cites conservative accounting and institutional skepticism about sustained high gold prices-a classic case of capitalist caution.

Read More

- Gold Rate Forecast

- Is Now the Time to Buy Bitcoin? Shocking Market Signals Unveiled!

- XRP: The Calm Before the Storm?

- Brent Oil Forecast

- Bitcoin’s Plunge: Are Traders Running for the Hills? 🤑💨

- X Accounts Go Rogue: The Flare Security Scare You Won’t Forget

- SEC’s Crypto Custody Circus: Who’s Guarding Your Digital Gold? 🎪💰

- Suspected Team Wallet Sent $47M of TRUMP to Crypto Exchanges: Dump Incoming?

- Who Owns Bitcoin ETFs Now? Shocking Top Holders Revealed! 😂

- Bitcoin’s Dramatic Dive: A Comedy of Errors and Accumulation! 💸😂

2026-02-26 20:27