Oh, Bitcoin, you fickle minx! Short-term holders are still clutching their pearls (and their losses) as the market does its best impression of a snail on a salt flat.

So, here we are, five months into this financial soap opera, and Bitcoin’s short-term holders are still staring at their screens like they’ve just been ghosted by their crypto crush. On-chain data? More like on-chain drama. Their positions are deeper in the red than a tomato at a vampire convention. Recent buyers are holding coins like they’re waiting for a bus that may never come-and at prices higher than today’s market value. Ouch.

Back in the day, this kind of slump would’ve been a neon sign flashing “BUY NOW, REGRET LATER!” But now? It’s more like a mixed-signal Tinder date. Lower leverage, softer ETF demand, and steady loss-taking are all whispering, “Slow your roll, honey.” A fast rebound? As likely as a Bridget Jones sequel without Renée Zellweger.

Short-Term Holders: Still Drowning in the Red Sea of Regret

Short-term holders, the market’s emotional rollercoaster riders, are feeling the strain. Their realized price is hovering around $87,000, while Bitcoin is lounging below like it’s on a permanent siesta. That gap? It’s the financial equivalent of a bad breakup-many recent buyers are still holding onto coins at a higher cost than today’s price. Cue the sad violin music.

Five months of losses? That’s longer than most of my relationships. STHs are basically in a crypto version of Bridget Jones’s Diary, except instead of Mark Darcy, they’re waiting for Bitcoin to text them back.

– Darkfost (@Darkfost_Coc)

Darkfost, the Sherlock Holmes of on-chain data, points out that the short-term MVRV ratio is at 0.78. Translation? An average loss of 22%. Recent entrants are basically holding crypto-shaped bags of air. Past bull markets would’ve turned this into a buying frenzy, but now? It’s more like a cautious coffee date. Five months of losses aren’t just a blip-they’re a full-blown sitcom season.

Spot Demand Takes the Stage After Leverage’s Dramatic Exit

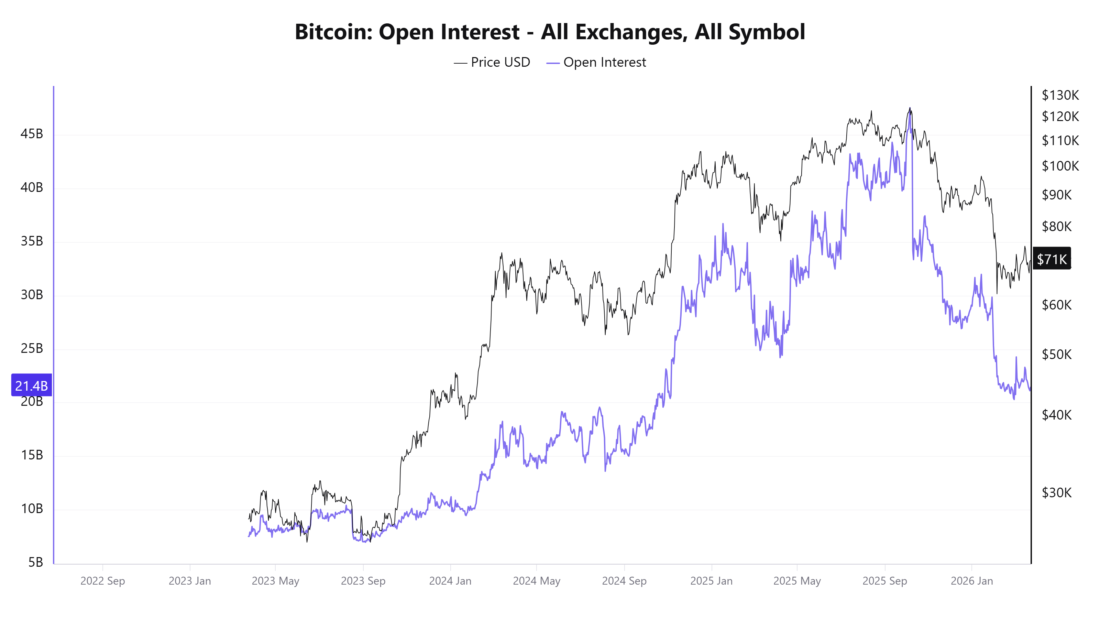

Derivatives data? It’s serving us a reality check. Open interest has plummeted from $45 billion to $21 billion-faster than a Black Friday sale. That’s a major flush of speculative positioning after Bitcoin’s $100,000 party. So, what’s left? A market less about leverage-fueled mania and more about real spot demand. Think of it as the difference between a one-night stand and a long-term relationship.

Image Source: CryptoQuant

ETFs, once the belle of the ball, are now posting outflows like it’s going out of style. But don’t panic-flows have stabilized, with modest weekly inflows like $167 million. It’s not a mass exodus; it’s more like a polite “I’ll just grab my coat and leave the door open for you.” Big players are stepping back, not running for the hills.

MVRV Recovery: The Holy Grail of Bitcoin Momentum

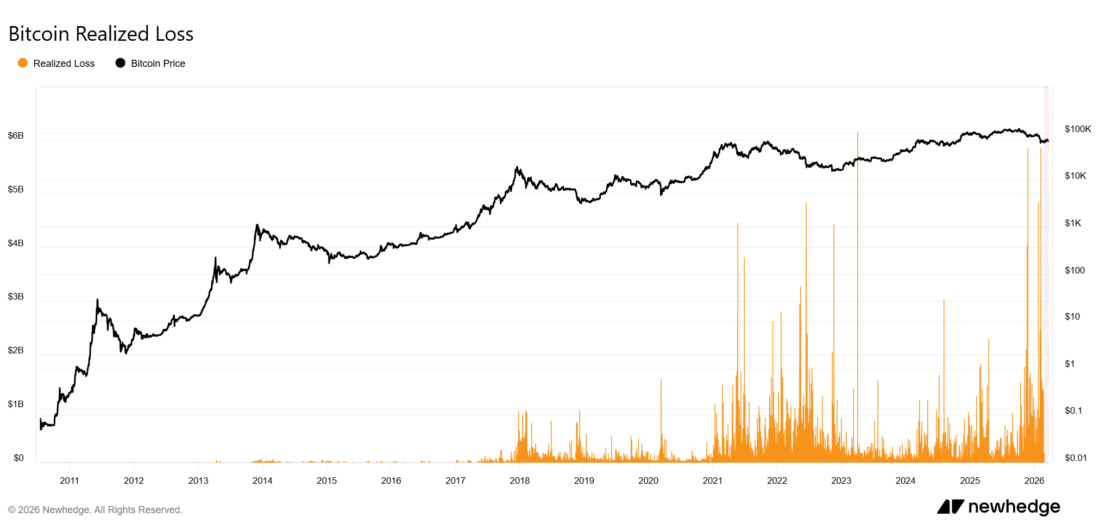

Realized losses are up, but they’re not exactly Titanic-level drama. No COVID crash or FTX-style meltdown here. Selling pressure? More like a drizzle than a downpour. Investors are accepting losses, but it’s a slow burn, not a bonfire. Think controlled capitulation, not a full-blown panic attack.

Image Source: NewHedge

If Bitcoin can reclaim $87,000, short-term holders might finally stop crying into their lattes. An MVRV above 1? That’s the equivalent of a “we’re back, baby!” moment. Stronger ETF inflows could be the institutional version of a second date, while a spike in realized losses might just be the final act of this financial drama.

So, will Bitcoin holders ever surface from this red ocean? Only time-and a lot of therapy-will tell.

Read More

- Pi Hotel Vietnam: First to Accept Pi Coin Payments in Real-World Transactions

- Silver Rate Forecast

- Gold Rate Forecast

- USD IDR PREDICTION

- The Quiet Rise of Ethereum: Is it Really Gone or Just Getting Started?

- USD COP PREDICTION

- USD TRY PREDICTION

- ZEC PREDICTION. ZEC cryptocurrency

- Why These 5 Meme Coins Could Crash or Cash Your Crypto Party in May 2025 🚀🐒

- Brent Oil Forecast

2026-03-24 18:07