The bond market is staring down oil shocks, political drama, and a looming Fed leadership shake-up-and the result is a Treasury market behaving like a caffeinated cat: twitchy, watchful, and very much not ready to relax.

Treasury Yields Jumpy as a Cat on a Hot Tin Roof Amid Oil Tensions and Fed Politics

U.S. Treasury yields are holding stubbornly high this week, with the benchmark 10-year hovering around 4.24% as of midday March 12. That’s roughly 18-20 basis points higher than a month ago-no small move in a market that normally celebrates stability like it’s a rare antique.

In bond-world terms, the message is simple: inflation worries are back at the party, and they brought oil prices as their plus-one.

Energy markets have been wobbling between tension and outright drama thanks to geopolitical risks involving Iran and shipping routes through the Strait of Hormuz. Oil briefly flirted with triple-digit levels earlier last week, and traders-who have the collective nerves of someone watching a horror movie through their fingers-are pricing in the possibility that higher fuel costs could seep back into consumer inflation.

For Treasury buyers hoping for a peaceful glide into lower yields, the timing could hardly be worse.

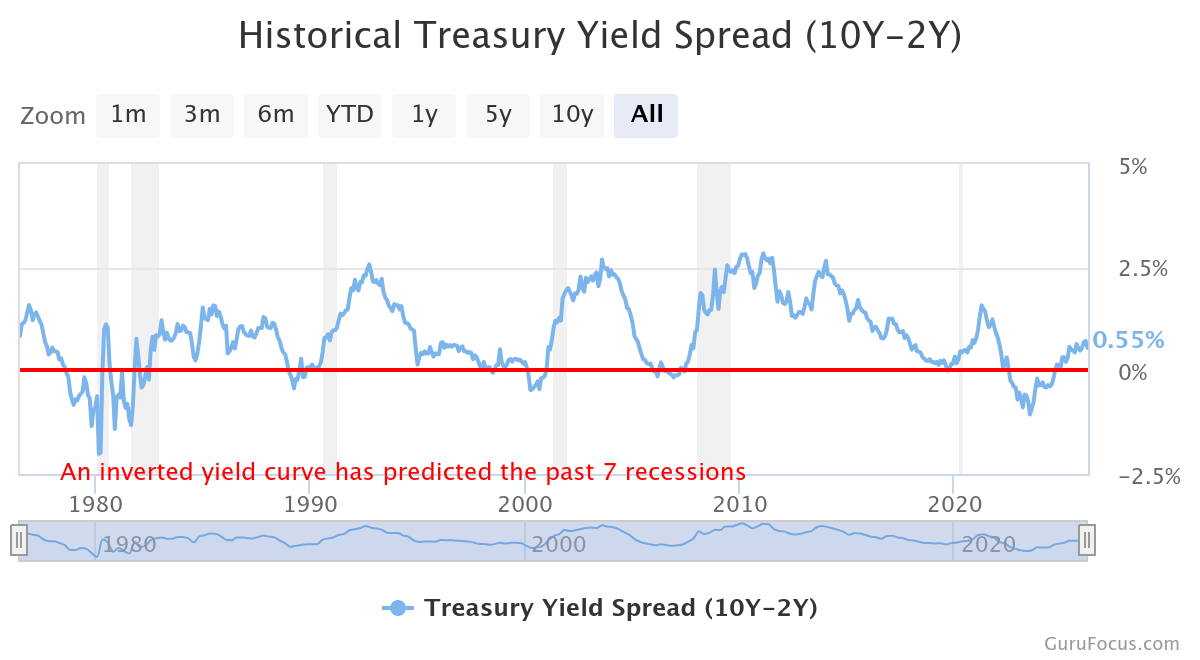

The yield curve has been steepening, with long-term Treasury yields rising faster than short-term ones. The 2-year note is sitting around 3.65%, while the 30-year bond has crept toward 4.88%. That leaves the spread between the 10-year and 2-year hovering near 0.59 percentage points-a signal that markets expect longer-term inflation to remain sticky even as the Federal Reserve hesitates to loosen policy anytime soon.

Translation: the bond market believes interest rates may stay elevated longer than Wall Street had hoped.

If investors were holding out hope that the Fed might swoop in with a string of rate cuts this year, the futures market has some news-and it’s not exactly comforting bedtime reading.

According to CME Fedwatch pricing, traders currently expect only one 25-basis-point rate cut in all of 2026. Just one. The first possible move isn’t even anticipated until September, and even that isn’t exactly locked in.

Markets are now staring down the March 17-18 Federal Open Market Committee meeting with a near-unanimous expectation that the Fed will keep rates exactly where they are. The odds of a hold are hovering around 99%, which in financial terms is about as close to “don’t bother setting an alarm” certainty as one gets.

Of course, monetary policy rarely unfolds in a vacuum. Enter politics, stage left.

Federal Reserve Chair Jerome Powell’s term as chair expires May 15, 2026, and President Donald Trump has already nominated former Fed governor Kevin Warsh to take the job. The nomination dropped earlier this year like a well-timed plot twist, and markets are still trying to figure out what it means for the future of interest-rate policy.

If confirmation were swift and tidy, investors might have already moved on. But tidy is not currently on the menu.

The Senate confirmation process has stalled, with Sen. Thom Tillis, R-N.C., blocking progress until a Department of Justice investigation into a renovation project at the Fed’s headquarters is resolved. The renovation, once a mundane bureaucratic detail, has suddenly become political theater worthy of its own streaming series.

Meanwhile, the White House has been openly pressing for faster rate cuts-an unusual level of commentary about central bank policy that markets are watching with the same curiosity normally reserved for a high-wire act.

Some investors believe a Warsh-led Fed could prove more open to easing monetary policy than Powell’s current stance. Others suspect the transition itself may create uncertainty that keeps bond yields volatile in the months ahead.

For now, the result is a Treasury market that’s pricing in a complicated mix of forces: persistent inflation worries, large government borrowing needs, and a leadership transition at the world’s most powerful central bank.

Meanwhile, the broader economy isn’t exactly immune to the consequences.

Mortgage rates remain parked in the neighborhood of 6.8% to 7.0% for a standard 30-year fixed loan, keeping the housing market in a holding pattern. Buyers are cautious, builders are cautious, and lenders are-well-also cautious.

If oil prices climb again or inflation data surprises to the upside, those borrowing costs could remain elevated even longer.

Looking ahead, markets are watching several near-term catalysts: next week’s Fed meeting and Powell’s press conference, new inflation data due April 10, Senate hearings tied to Warsh’s nomination, and-perhaps most unpredictably-the trajectory of energy markets.

Because if the past few years have taught bond traders anything, it’s this: just when the economic script seems predictable, someone flips the page and adds another twist.

And right now, the Treasury market is reading every line.

FAQ 🔎

- Why are Treasury yields rising in 2026?

Rising oil prices, inflation concerns, heavy government borrowing, and uncertainty over the Federal Reserve’s leadership transition are pushing Treasury yields higher. - What is the current 10-year Treasury yield?

As of March 12, 2026, the 10-year U.S. Treasury yield is trading around 4.23%-4.25%. - When could the Federal Reserve cut interest rates again?

Markets currently expect the first potential rate cut no earlier than September 2026, with only one 25-basis-point cut priced for the entire year. - Why does Jerome Powell’s term matter for bond markets?

Powell’s chair term ends May 15, 2026, and the nomination of Kevin Warsh as successor introduces policy uncertainty that could influence interest-rate expectations and Treasury yields.

Read More

- Silver Rate Forecast

- Polymarket’s 3.14% Pie: A Slice of Genius or Just Crumbs?

- Gold Rate Forecast

- Brent Oil Forecast

- Coinbase’s OCC Nod: Not a Bank, Just A Trust-Big Moves Ahead!

- ONDO PREDICTION. ONDO cryptocurrency

- Claude’s ID Fiasco: Anthropic’s Latest Farce in AI Theatre

- XRP’s Institutional Comeuppance: Finally, a Seat at the Table

- Bitcoin at 75k: The Trigger That Could Unleash a Rally

- Crypto’s Last Gasp: Lummis Pleads, ‘Act Now or Regret Eternally’

2026-03-12 20:27